The Challenge: Resolving the Space-Cost Paradox in Mass-Market Retail

While premium supermarket chains engage in fierce bidding wars for expensive anchor-tenant allocations within luxury urban shopping malls, Econsave has quietly dominated the Malaysian mass-market retail landscape through a radically divergent physical model. Operating under the legendary, hyper-focused pricing architecture of "Bandingkan Harga Kami" (Compare Our Prices), Econsave's entire corporate infrastructure is built upon the ruthless minimization of structural overhead costs. To protect their razor-thin margins and pass massive wholesale savings directly to the consumer, they bypass traditional shopping mall ecosystems entirely, opting instead for massive, standalone warehouse formats positioned deep within high-density suburban fringes.

However, sustaining this low-cost leadership model requires a highly specific, mathematically rare set of spatial and economic conditions. Expansion teams cannot simply select any available suburban plot; they must constantly solve a complex equation that balances physical land constraints with strict demographic minimums. This presents two profound micro-geographical challenges:

- The Space-Cost Dilemma: Navigating Zoning Arbitrage

Econsave's operational blueprint demands massive horizontal square footage. Unlike vertical mall tenants, a standalone hypermarket requires a sprawling single-level warehouse layout coupled with extensive surface-level parking lots to facilitate frictionless, high-volume consumer loading. Securing this amount of real estate within urban centers carries prohibitive rental or acquisition costs that would immediately break the brand's low-overhead economic model. The expansion team's challenge is to execute precise "Zoning Arbitrage"—identifying large parcels of land priced at industrial-level baselines, but legally and logistically viable for commercial retail development. - The 10-Minute Isochrone: Driving Density Over Raw Distance

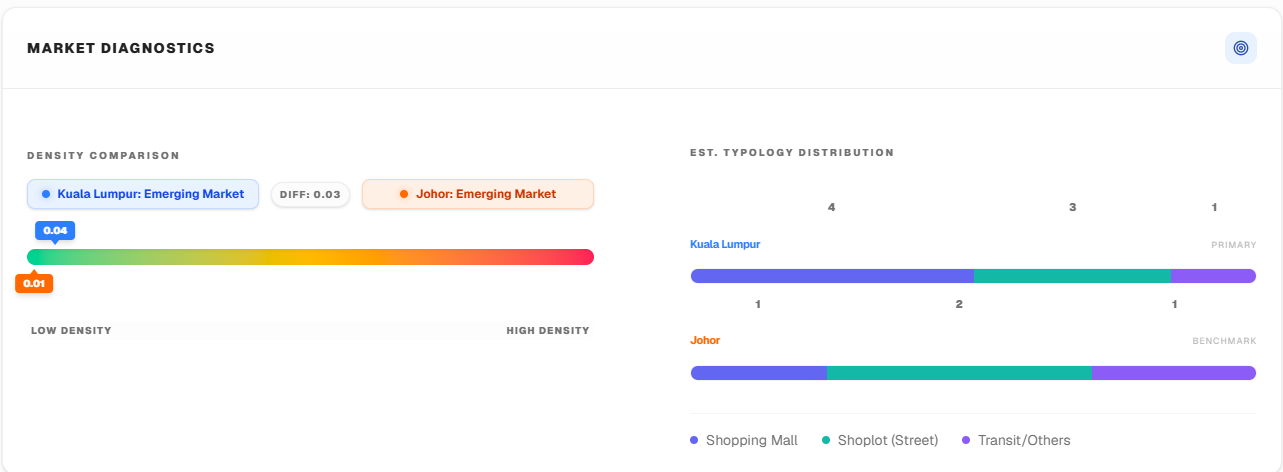

Acquiring cheap land on the deep periphery of a city is simple, but cheap land is economically useless if it sits in a demographic vacuum. For mass-market retail, profit is entirely driven by absolute volume. This cheap, industrial-priced land must be perfectly enveloped by a dense, high-yield consumer catchment—specifically sitting within a strict 10-minute driving or riding radius (isochrone) of massive B40 and lower-M40 residential populations. The core spatial hurdle is locating the precise geometric center where cheap land directly intersects with a critical mass of over 100,000 price-sensitive shoppers. - The CAPEX Finality of Standalone Footprints

When a premium grocer pulls out of an underperforming shopping mall, the landlord absorbs much of the structural loss, and the brand can relocate with limited real estate friction. For a standalone warehouse operator, however, site selection carries an absolute finality. Developing a dedicated warehouse represents a massive, irreversible Capital Expenditure (CAPEX). If the surrounding suburban demographics shift, or if traffic access is throttled by poor infrastructure planning, the brand is left holding an unadaptable, underperforming industrial asset. De-risking these high-stakes capital deployments requires a deep, data-driven synthesis of land classification, infrastructure pipelines, and highly granular population density modeling before a single brick is laid.