The Challenge: The Rent vs. Footprint Equation in Mega-Retail

Mega-retailers like MR DIY have not merely participated in the Malaysian retail landscape; they have fundamentally redefined it as undisputed "Category Killers." Their economic moat is built on overwhelming consumers with an exhaustive variety of inventory—routinely exceeding 15,000 to 20,000 active SKUs. To physically house and merchandise this massive product matrix, these operators require colossal floor plates, typically consuming 10,000 to 20,000 square feet per outlet.

This extreme spatial requirement creates a brutal tension at the core of their unit economics. Unlike high-margin luxury boutiques, a mega-hardware and lifestyle retailer relies on high-volume, low-ticket transactions. Expansion teams are consequently trapped in a continuous, high-stakes balancing act between necessary scale and commercial real estate economics, facing three distinct spatial dilemmas:

- The Prime Real Estate Trap: The OPEX Crush

In traditional retail, the ground floor of a Tier-1 shopping mall or a prime high-street corner is the ultimate prize. For a mega-retailer, it is financial suicide. Securing 15,000 square feet at premium, ground-level per-square-foot (psf) rental rates completely destroys the brand's profitability matrix. The Revenue Per Square Foot (RPSF) generated by RM 5 household hardware simply cannot sustain the exorbitant monthly Operating Expenses (OPEX) of Tier-1 zoning. The sheer gravity of the rent instantly crushes the margin before a single item is sold. - The Accessibility Drop-Off: The Death of the "Impulse Buy"

The mathematically obvious solution to high rent is retreating to industrial parks or deep suburban warehouse districts (the Econsave model). However, this introduces a fatal flaw: the destruction of the pedestrian slipstream. While MR DIY serves as a destination for specific needs, a massive percentage of its revenue is generated through spontaneous, visual impulse buys. Moving to a sterile, isolated industrial zone strips the brand of organic foot traffic. They require the massive square footage of a warehouse, but they critically depend on the high-frequency consumer footfall of a premium commercial artery. - The Search for "Secondary-Node Arbitrage"

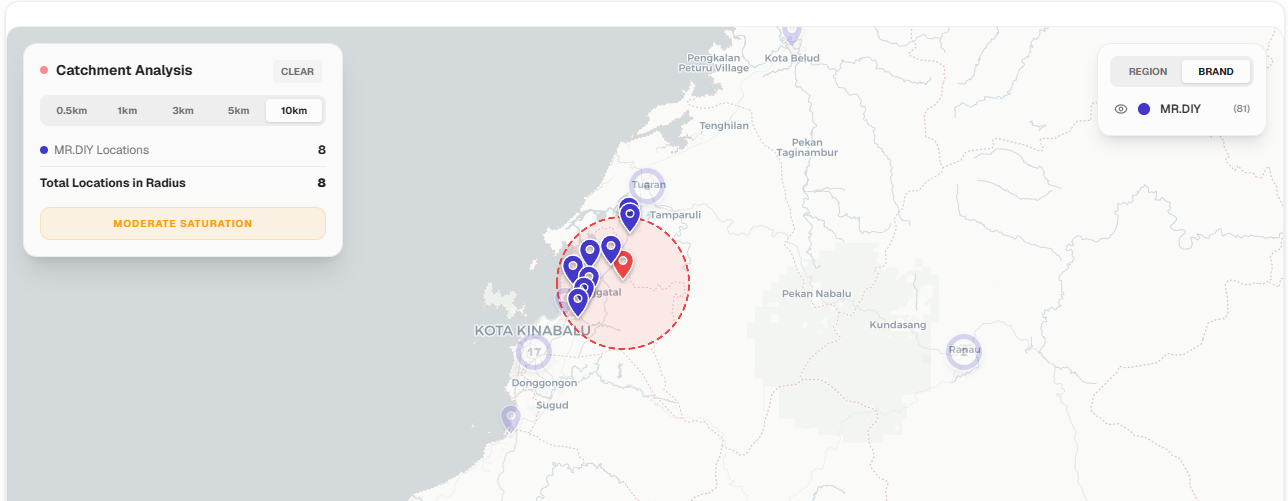

The survival and hyper-growth of this model depend entirely on executing perfect "Spatial Arbitrage." Expansion teams must hunt for "dead spaces" within high-traffic zones—such as the basement levels of bustling malls, abandoned anchor-tenant spaces on the 3rd floor, or oddly shaped rear-facing lots in mature commercial blocks. These specific units offer massive square footage at deeply discounted, Tier-3 rental rates, yet they still sit within a 2-minute walking radius of Tier-1 pedestrian density. Identifying these hidden, highly specific "Secondary Nodes" without comprehensive geospatial intelligence is akin to finding a needle in a metropolitan haystack.