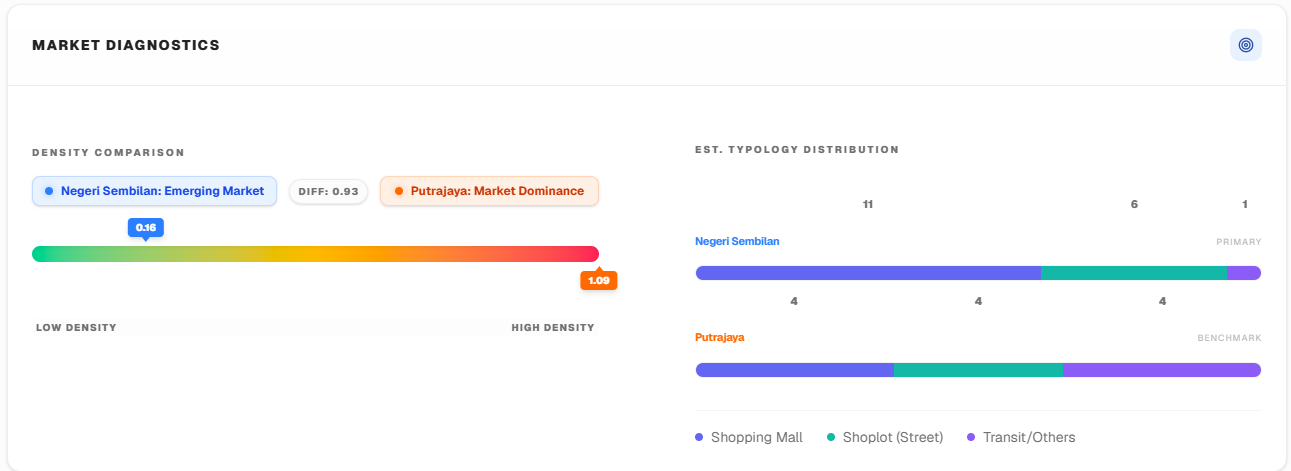

The Challenge: Measuring True Territorial Dominance in a Zero-Sum Duopoly

The Malaysian health-and-beauty (H&B) retail sector is defined by a relentless, decades-long duopoly between Watsons and Guardian. Operating as the ultimate anchor tenants for any commercial ecosystem, these two titans have effectively commoditized the product layer. Because their SKUs, pricing strategies, and promotional cycles are remarkably symmetrical, the battleground has shifted entirely away from the shelf and onto the map. This is a game of pure, zero-sum spatial warfare, where geographical convenience and micro-location dominance are the only remaining differentiators.

When two competitors each control vast networks of hundreds of nationwide outlets, macro-level statistics (such as total state-wide store counts) become dangerously obsolete vanity metrics. Expansion teams are no longer just looking for "good locations"; they are fighting for grid-level supremacy against a heavily armed rival. This creates three highly complex geospatial challenges:

- The Proximity Paradox: Decoupling Shared Catchments

In highly matured urban nodes like the Klang Valley, expansion teams face the "Proximity Paradox"—a retail manifestation of Hotelling's Law. Watsons and Guardian are frequently located literally next door to each other, or strategically positioned within the exact same shopping mall corridor. In these hyper-clustered environments, they share the exact same macroscopic footfall. The critical challenge for spatial analysts is uncoupling this shared data: how do you mathematically measure which brand is actually winning the micro-catchment? Winning here requires measuring microscopic friction—storefront visibility, walking vectors, and localized intercept angles—to determine who actually captures the pedestrian before they cross the competitor's threshold. - Regional Blindspots and "White Space" Mapping

As Tier-1 urban centers reach absolute saturation and diminishing returns, the frontline of this duopoly has aggressively expanded into Tier-2 states and emerging semi-urban districts. However, corporate expansion teams often suffer from severe "Regional Blindspots." Relying on generalized demographic data fails to reveal the granular reality of a competitor's localized monopoly. The strategic mandate is to execute precise "White Space Mapping." Expansion managers must algorithmically identify geographical voids—dense residential pockets that possess sufficient disposable income for personal care spending, but currently have absolute zero coverage from either brand. Securing a lease in these validated white spaces grants critical first-mover monopoly advantages. - True Territorial Yield vs. Aggregate Scale

Comparing aggregate store counts creates a false sense of security at the boardroom level. Having 50 stores in a state means nothing if 40 of them are locked in low-yield, hyper-competitive zones, while the competitor holds 30 highly optimized, high-yield localized monopolies. The ultimate spatial challenge is transitioning from simply counting real estate to calculating True Territorial Yield. Brands require the intelligence to measure defensive market share at the sub-district level, ensuring that every new Capital Expenditure (CAPEX) deployment actively degrades the competitor's localized dominance rather than just adding a pin to a map.